Mortgages are stressful. They are one of the most important contracts you’re ever going to sign and you really have no one looking out for you except yourself.

Pre-Approval

First of all, make sure that you get pre-approved before you start shopping for a house. As I’ve mentioned in other posts, this will help you establish your buying limit and also avoid any stress during bid time.

Research

I’ve done a lot of research on mortgages and I’m not sure I’m any less confused. I am, however, more terrified. I’ve read enough horror stories about collateral mortgages and penalty charges to make me want to rent forever (thanks, CBC). Or save up until I can just buy a house outright.

After a lot of research, I was able to find the basics online: closed v. open mortgages, fixed v. variable interest rates, and collateral v. conventional mortgages. I also asked around and, to my surprise, most people claimed they hadn’t done any research before signing and have no idea what advice to give. Some didn’t even know that they had a collateral mortgage.

So how do you confirm that you’re not getting royally screwed? Well, you can’t. But you can make sure you’re getting less screwed than just blindly signing on the dotted line.

Negotiating your mortgage

Most of the people I spoke to about their mortgage experience said the same thing: “We were just happy that someone was willing to give us a mortgage. So we took whatever they gave us.” Really? Really?!

Let’s do some simple math. If you’re purchasing a $500,000 house and have 20% down, your mortgage amount is $400,000. At 3% interest (which will inevitably increase over the 25 year period), you will have given the bank approximately $168,000 in interest. If interest rates climb to even just 5%, that amount increases to almost $300,000. So you have every right to make sure that you’re happy with your contract. Also, don’t be lazy. That’s a lot of money to be lazy about.

I had a lot of trouble finding any clear details on how to avoid major screw-tactics in a mortgage agreement. Until last night.

The Globe and Mail posted a great article in October with the ultimate mortgage checklist. I suggest using this list and going through the document to see if you agree or have further questions for your mortgage lender. I don’t know if it covers everything, but it does claim to be the ultimate checklist.

Paying your Mortgage

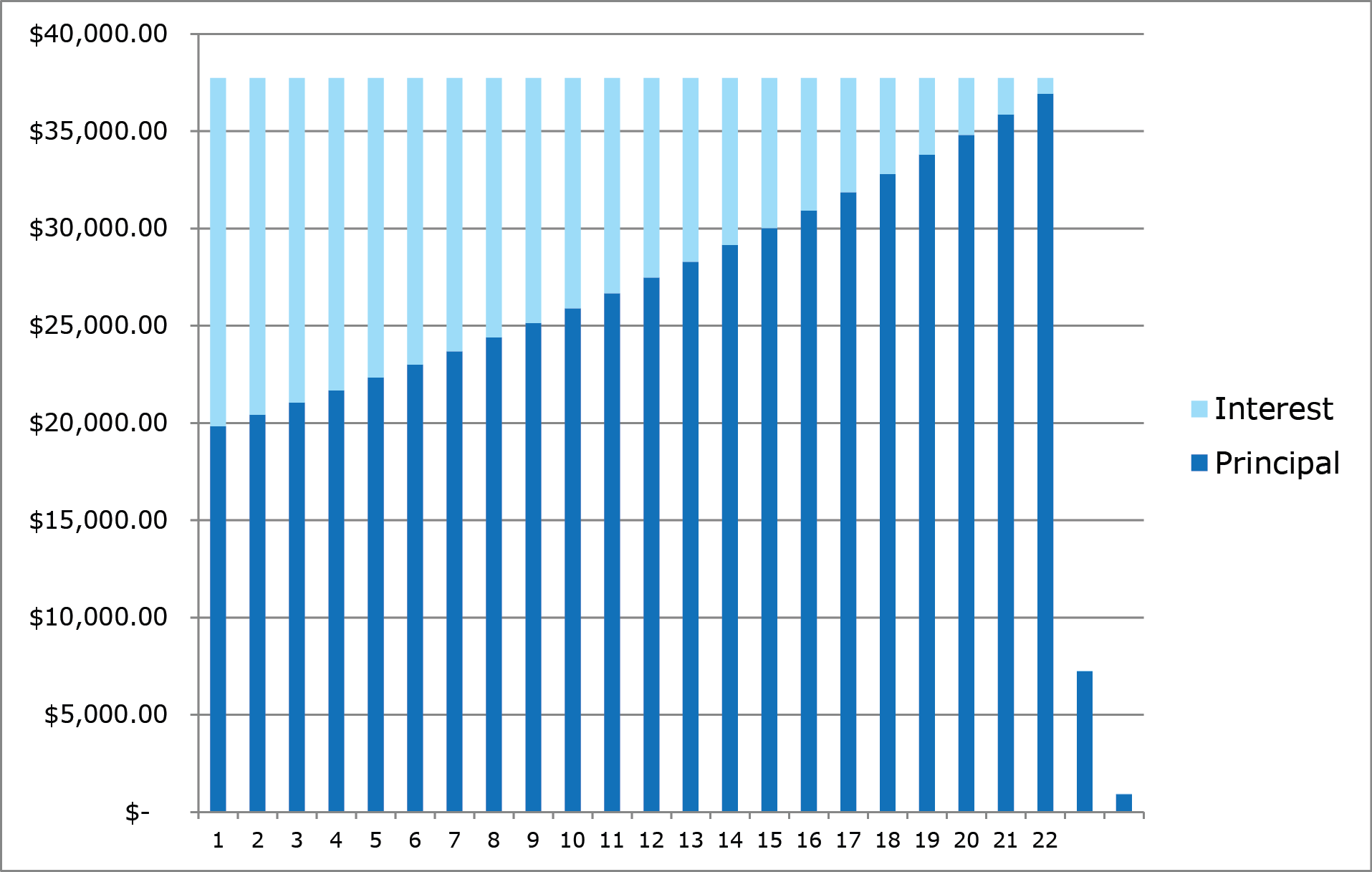

There are several ways to pay your mortgage. You can pay it monthly, bi-weekly, accelerated bi-weekly, and so on. There are several great calculators online that let you play around with these options, so I won’t get into too much detail here. But the basic rule is, the more you pay and the more often you pay, the less you pay in interest. So if you can’t afford to pay more each payment (most banks let you increase your payments and/or pay a lump sum payment every year – these amounts differ by bank), then at least increase your frequency.

We chose accelerated bi-weekly. This essentially means that we’re paying the same amount (the bi-weekly amount is just half of the monthly amount), but because it’s every 2 weeks, you get an extra couple of payments in. This is why:

Monthly Payments:

12 months = 12 payments

Bi-Weekly Payments:

52 weeks = 26 payments

Since 12 x 2 is 24, the 26-payment option means that you’re paying an extra 2 payments per year. Maybe it doesn’t seem like much, but it adds up over the life of the mortgage. Plus, this entire amount goes to the principle (not the principle + interest), so you’re paying down more of your actual debt faster. It also means that you’ll pay off your mortgage in 22 years and change, versus 25 years.